Image source: Getty Images

Since the start of the conflict in the Middle East, shares in BP have set a new 52-week high. And with the oil price showing no sign of dropping, there could be more records broken soon.

However, there’s another stock that’s risen more over the past four weeks. The two are like chalk and cheese, so how can this non-energy group be doing so well given the current global uncertainty? Let’s take a closer look.

Who?

The RELX (LSE:REL) share price has been rising steadily.

Today (16 March), shares in the FTSE 100 information and data analytics group are changing hands for 17% more than they were a month ago. Over the same period, BP’s share price is up 16%.

It follows a dramatic fall in early February, when investors sent RELX’s stock price 14% lower on the day that Anthropic announced it had developed an add-on for its Claude artificial intelligence (AI) tool. Although not directly replicating any of the services provided by RELX, there was a fear that it could empower legal teams and disrupt the business models of established companies operating in the sector.

Other data and software stocks also suffered. Since then, a number of observers have come to the defence of the group and the sector in general.

Nvidia’s boss, Jensen Huang, recently said: “I think the markets got it wrong.” He reckons AI agents will rely on the data that these companies own rather than make their products and services obsolete.

Finsbury Growth and Income Trust has significant positions in many data companies, including RELX. Its fund manager, Nick Train, claims they all have “a credible opportunity to bring AI-enhanced services to their customers, an opportunity based on their ownership of data assets that are not available to emerging large language models (LLMs) like ChatGPT or Anthropic.”

Huge volumes of proprietary data

And when it comes to data, RELX has lots of it. For example, its Scientific, Technical, and Medical division makes available 105m publications to subscribers. Separately, legal professionals have access to over 200bn documents. The group claims to analyse 130bn transactions annually.

Although impressive, this makes it particularly vulnerable to a cyber attack or data privacy breach.

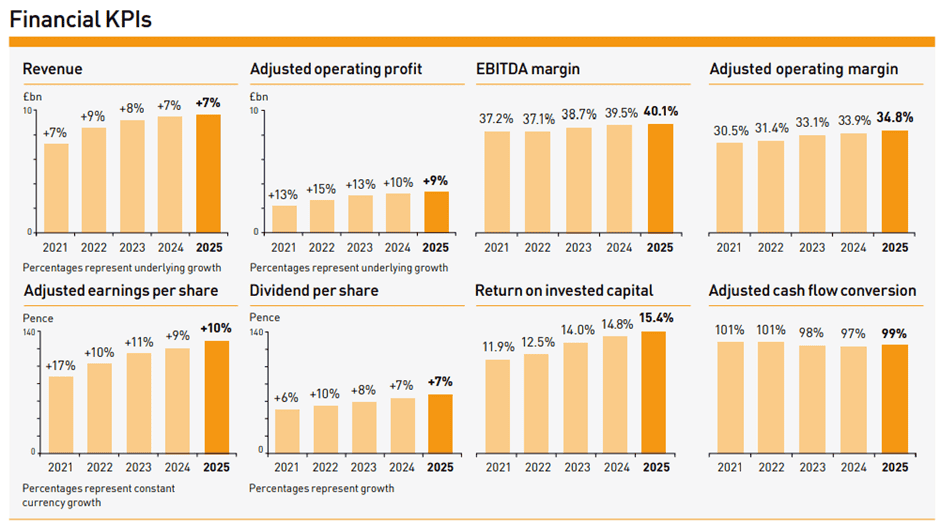

But at the moment, RELX sees AI as an opportunity to enhance customer value and reduce costs. Indeed, it was spending heavily on AI long before it became fashionable. This has helped drive its key financial measures higher during its past five financial years.

In particular, its focus on business customers — where the emphasis is more on quality than price — has helped it increase its EBITDA (earnings before interest, tax, depreciation, and amortisation) margin.

And I reckon the recent pullback in the group’s share price could make it an excellent buying opportunity to consider.

Over the past five years, the stock’s average (median) price-to-earnings ratio has been approximately 30. Based on its 2025 earnings per share (EPS) of 112p, it’s now under 23.

Hopefully, the war will end soon. And when it does, energy prices are likely to fall back towards pre-conflict levels. In these circumstances, BP’s share price is probably going to suffer but I’m confident that RELX’s will continue to go in the opposite direction.