Image source: Getty Images

Passive income could be your ticket to a retirement beyond the measly State Pension amount of £231. With compounding on your side, even modest ISA savings, built steadily over time, could generate a reliable income to top up your retirement income.

Crunching the numbers

If you want £924 a month in today’s money when you retire, inflation means you’ll need more than that in the future. Assuming 3% annual inflation, in 25 years the same purchasing power would require around £23,200 a year.

Using the 4% withdrawal rule, a pension pot of roughly £580,000 would be needed to generate that income.

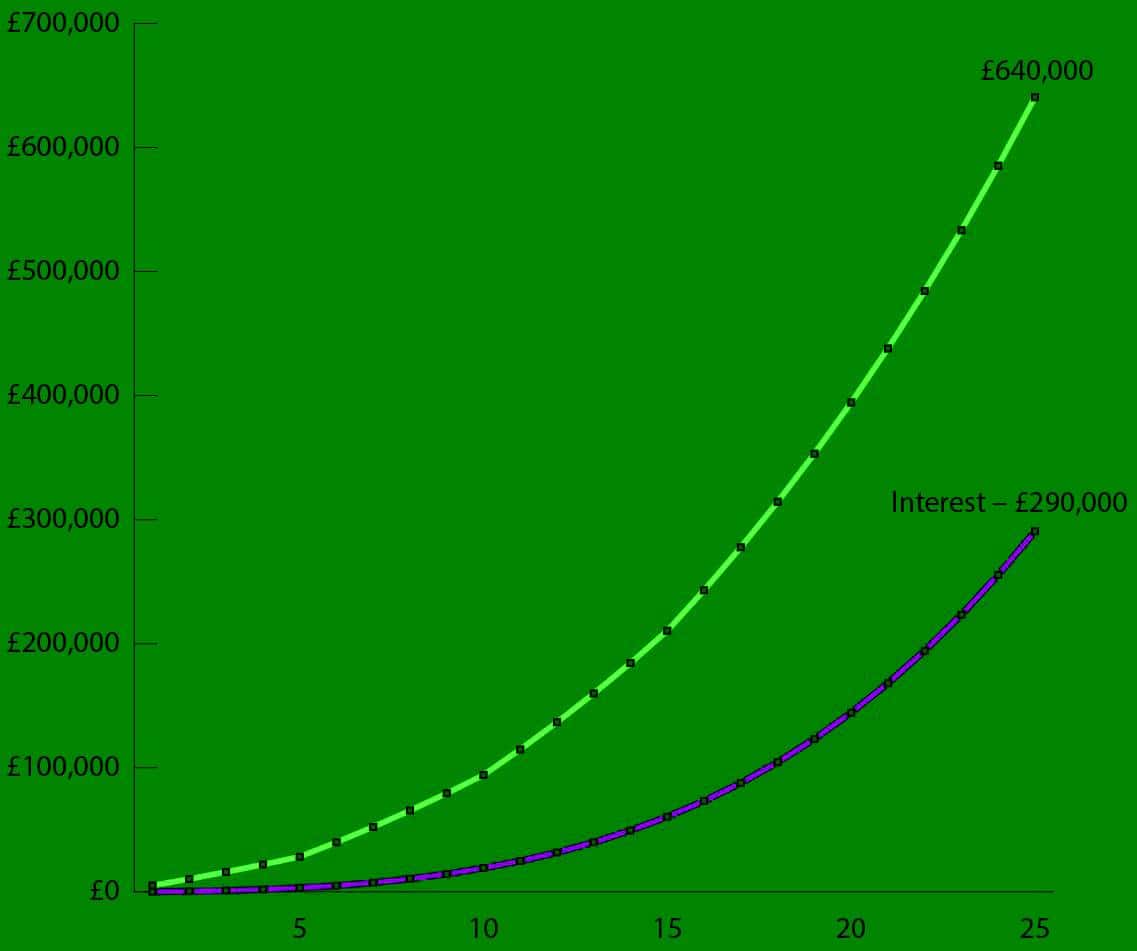

Let’s assume an individual has a 25-year investment horizon and will increase their yearly ISA contributions according to the table below.

| Tiered years | Yearly ISA contribution |

| 1-5 | £5,000 |

| 6-10 | £10,000 |

| 11-15 | £15,000 |

| 16-25 | £20,000 |

The following chart models these contributions, assuming a modest 6% annual return. As shown, the individual not only surpasses their target but also demonstrates the power of compounding, which alone contributes around 45% of the final total.

Chart generated by author

In order to reach that sizeable pot size, my preferred choice is a blend of both growth and dividend shares. One stock in the latter category that I think investors should consider is Legal & General (LSE: LGEN). Its trailing dividend yield is 9.2%, comfortably ahead of the 6% target.

Dividend sustainability

Over the past 10 years total shareholder returns have amounted to 83%. But of course it’s the future that matters.

Dividend cover currently stands at 0.94, meaning that earnings don’t fully cover the payout. That naturally raises questions for an income stock.

For insurers, cash dividend cover is usually the real safety net. Even when profits fluctuate, steady operating cash flows from premiums and investment income normally back up the dividend.

But last year was an exception. The company reported negative operating cash flow of £4.4bn, leaving no cash cover for the payout. On the face of it, that looks like a flashing warning light.

Why I still think the dividend is safe

Despite that, I think the risk of a cut still looks low. That’s because what really underpins insurer dividends isn’t short-term cash flow – it’s the capital the business reliably produces to fund both distributions and growth. It’s measured as Solvency II operational surplus generation (OSG).

OSG is expected to rise around 5% in 2025, comfortably above the planned 2% increase in dividends per share.

The forthcoming £1bn share buyback adds further support. By reducing the share count, it cuts the annual dividend bill by roughly £100m, further bolstering OSG.

Bottom line

I’ve long held Legal & General shares in my Stocks and Shares ISA for their reliable, market-beating dividends.

Last year was challenging, yet the company still grew the cash cost of its dividend. Its long-term growth drivers remain solid.

The real engine is pension risk transfer. Trustees rely on the insurer to derisk final salary schemes; a highly lucrative, expanding market with a total addressable market set to hit £1trn over the next decade. This combination of reliability and growth could make the shares a solid source of passive income for patient investors.