Image source: Getty Images

With interest rates set to fall and geopolitical tensions sending shivers through markets, the outlook for UK shares is changing.

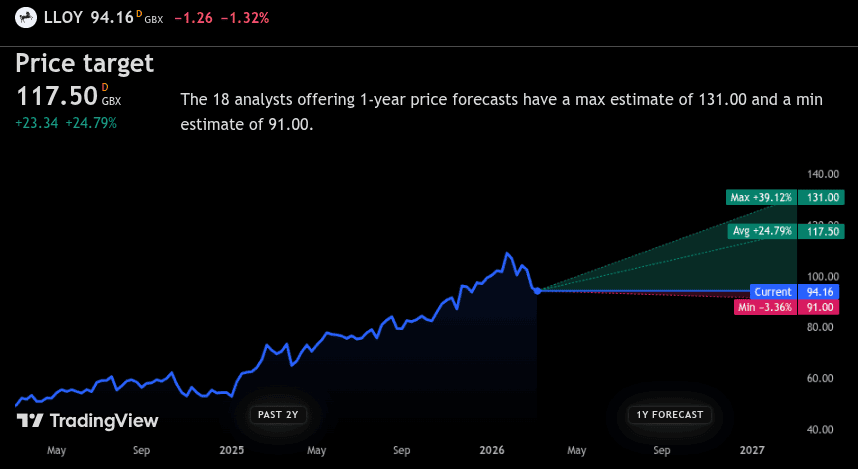

With Lloyds‘ (LSE: LLOY) shares often considered a bellweather for the domestic market, I decided to see where analysts think they may be heading in the coming year.

Looking ahead

Analysts following Lloyds have an average 12‑month price target of 117.5p, which would be a 24.92% gain from today’s level. If that played out, £1,000 would grow to roughly £1,250 just from the shares alone. Add the 6% dividend yield and the total return could be close to 30%, or around £1,300 (before dealing costs and tax).

On the optimistic end, some analysts think the price could climb about 39.27%. In that case, £1,000 could grow to roughly £1,390 from share price alone, or nearer £1,450 including dividends.

At the pessimistic end, the gloomiest forecast is for a 3.29% price fall. Even then, the dividend could still leave an investor roughly flat or slightly ahead over the year.

To get a better idea of where it may be headed, I took a closer look.

Key fundamentals and dividends

Over the last five years, Lloyds’ share price is up around 125% — a pretty strong rally for a mature bank stock. But revenue is the real story here, and a clear indication of the benefits of a higher interest rate environment. It has more than doubled since 2022, rising from £26.2bn to £65.55bn.

What does this mean for shareholders? Well, return on equity (ROE) isn’t spectacular — it sits just above 10%, broadly in line with many large lenders. But where Lloyds typically wins is income.

The stock currently offers a dividend yield just below 6%, and payouts use only about 52% of earnings — so they’re well covered. Plus, it’s backed up by 12 years of uninterrupted payments, adding a degree of reassurance for those targeting passive income.

Macro backdrop and risks

As a largely domestic bank, Lloyds is heavily exposed to the health of UK consumers and businesses. A key growth driver in recent years has been interest rates. But following several cuts, the Bank of England base rate now sits around 3.75%, with further cuts expected.

This presents a mixed picture for Lloyds. Lower rates can squeeze lending margins, but they also support the housing market and keep bad debts in check. But if the economy slows or unemployment rises faster than expected, profits could come under pressure.

Still, it’s managed to pair dividends with sizable share buybacks.

Final thoughts

For a UK investor looking to open a new ISA in April, Lloyds still looks attractive. It’s a big, familiar bank with a chunky dividend yield and analyst expectations are for modest share price growth over the next year. The bank’s profitable, well capitalised and returning plenty of cash to shareholders.

However, this is still a cyclical share tied closely to the fortunes of the UK economy. Anyone buying today should be ready for bumps along the way – especially if growth disappoints or the housing market turns.

For investors comfortable with those risks, it offers income plus some potential positive price action. But it’s just one of several high-yielding FTSE shares to consider on the UK market today.