Image source: Getty Images

I worked out the dividend yield on my Stocks and Shares ISA recently. Overall, it comes in at 1.81%, which might be a surprise. That’s unlikely to excite passive income investors.

But there’s a very good reason why I’m not chasing a higher yield in my portfolio.

Why’s the yield so low?

In general, the stocks I own in my ISA don’t have huge dividend yields. But that’s not because they aren’t making money – they are.

Rather than returning that cash to shareholders though, the businesses retain it internally. And I’m generally a big fan of them doing this.

To see why, think about what happens to the cash retained by a company. It doesn’t go to the CEO or get spent on the staff Christmas party. Instead, it gets invested by the business. And it can be used to open new sites, develop products, or even acquire other firms.

Importantly, these can generate better returns than I can find in the stock market. So it’s better for me if they use their cash internally.

An example

A good example is Bunzl (LSE:BNZL). The company does pay a dividend, but it’s what happens with the rest of its net income that I’m interested in.

The firm uses the cash it retains to finance its growth. And a big part of this is buying other businesses that can expand its operation.

There are always risks with investing. And one is the danger of paying too much to acquire a new business. As with any investment, it’s impossible to eliminate the risk entirely. But there are some key metrics to pay attention to.

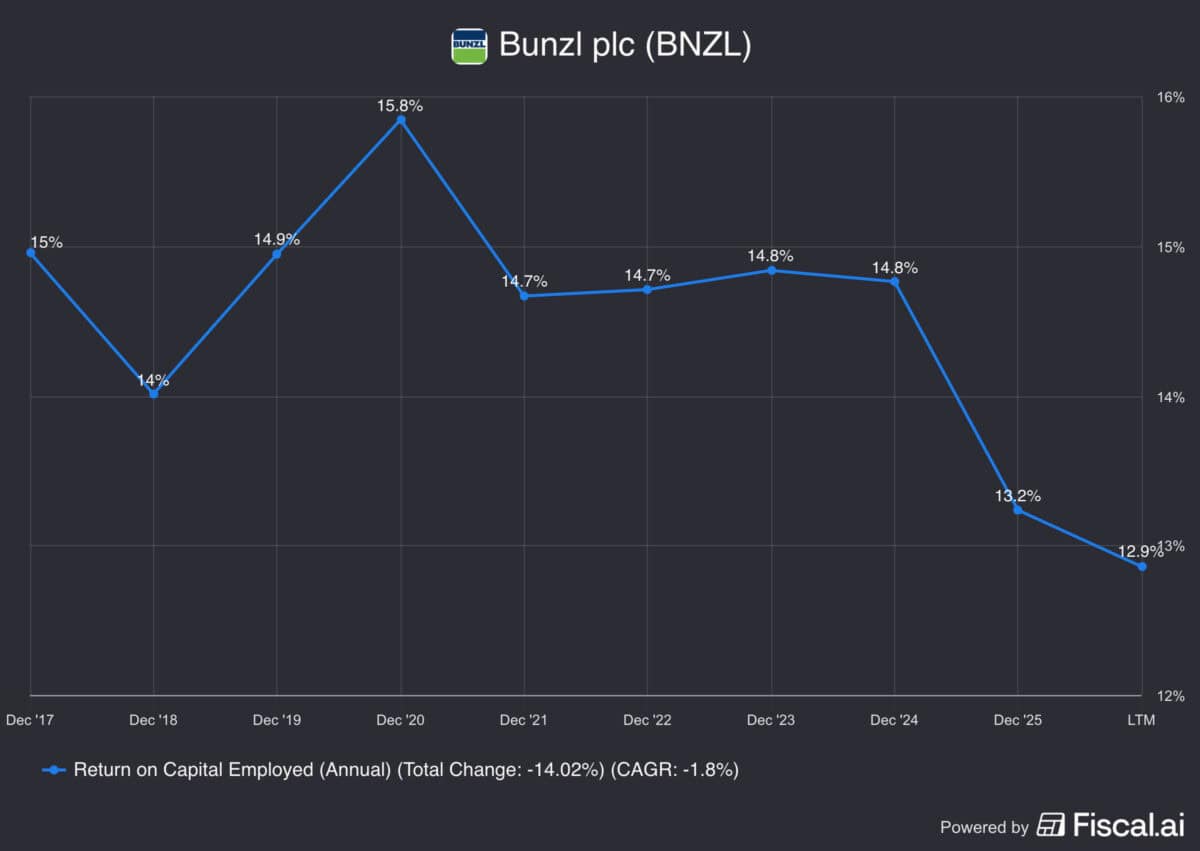

One of these is the return on capital employed. This measures how much profit the firm is generating relative to the cash it retains.

What to look for

There are a couple of things to note about Bunzl’s returns on capital employed. The first is that it’s consistently been pretty high.

In recent years, the metric’s been well above 12%. And it isn’t easy to find that kind of return in the stock market elsewhere right now.

The metric’s fallen in recent years. A big part of this is deflationary pressures following the pandemic lasting longer than expected.

Those however, look largely temporary to me. And I think Bunzl has a lot of scope for future acquisition growth still to come. A highly fragmented market means a large number of potential targets. And I expect the firm to make the most of this.

Building wealth

Building wealth involves compounding returns at high rates over a long time. But while reinvesting dividends is one way of doing this, I don’t think it’s my best way. By reinvesting dividends, I think I can manage a return of around 7%. That’s not bad, but it’s well short of what the likes of Bunzl achieve.

Despite some recent difficulties, the firm’s still earning over 12% on its capital. And that’s the number that matters to me, not the dividend yield.

Source link