Image source: Getty Images

I’ve always looked at the bottom of the performance league tables when on the hunt for value shares. Here, it’s sometimes possible to find a well-known name that’s fallen on hard times.

But the key to value investing is to identify those struggling due to a short-term issue, something that’s unlikely to last for very long. Otherwise, there’s nothing to stop a company’s share price falling further. With this in mind, could this familiar name on the FTSE 100 begin a comeback soon?

Who are we talking about?

JD Sports Fashion‘s (LSE:JD.) a staple of Britain’s high streets and retail parks. However, the self-styled ‘King of Trainers’ is struggling.

Although it’s grown in recent years by buying more overseas stores, its like-for-like sales are falling. The retailer’s most recent trading update revealed a 2.1% drop for the 48 weeks to 3 January, compared to the same period a year earlier.

When its full-year results are released, analysts are expecting a similar fall. And they’re predicting a drop of 0.7% for the 52 weeks ending 30 January 2027 (FY27).

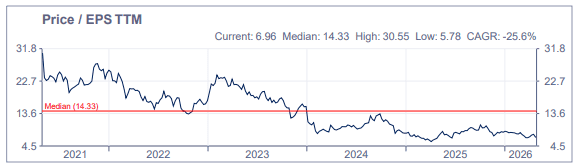

Clearly, this lack of growth explains the group’s disappointing share price performance. Indeed, the company’s now in danger of being relegated from the FTSE 100.

More bad news

On 22 April, the City had another reason to put the boot in with the surprise announcement that the group’s chair, Andrew Higginson, would leave in the summer. Even though the reasons are unclear, I believe investors over-reacted.

The group’s shares fell 3.9% wiping over £140m off its market-cap. With remuneration of £480,000, investors value Higginson at over 290 times his earnings!

That’s massively more than the group itself. In fact, the stock’s historic price-to-earnings (P/E) ratio is close to its five-year low and comfortably below its average (14.3) over this period.

As we move into the next phase of our journey, our focus on business discipline and cashflow leaves JD well-placed to deliver the value it unquestionably represents

Andrew Higginson, chair, JD Sports

On the other hand…

Yet despite its lack of growth, the group remains cash generative and, excluding leases, is in a net cash position.

Analysts are expecting FY27-FY28 free cash of over £900m. With no plans to expand, this should leave plenty of money to spend on redeveloping and refreshing its existing stores. This could be the catalyst to get the group’s share price moving in the right direction again.

Analysts are forecasting earnings per share as follows:

- 11.37p (FY26).

- 11.38p (FY27).

- 12.50p (FY28).

Trading at just 5.5 times forecast (FY28) earnings, the stock appears incredibly cheap. In theory, investors are likely to be attracted to stock with a low P/E ratio. However, with a lethargic top line it’s hard for investors to get excited, despite the group being profitable and cash generative. Momentum’s so important in the world of investing.

As a shareholder, I find this lack of progress frustrating. But I’m not giving up on the company. With its strong brand, increased exposure to North America, and the enduring appeal of the athleisure market, I think it will get back on its feet soon.

That’s why I think it could be considered by long-term investors looking to buy a cheap share at a rock-bottom price.

Source link