Image source: Getty Images

When it comes to FTSE 100 stocks, Legal & General (LSE:LGEN) is no Rolls-Royce. There isn’t a 1,000% share price surge or skyrocketing profits. No sexy SMRs or demand for AI data centre power.

Legal & General (L&G) sells insurance, pension products and manages assets. It was founded by lawyers in 1836, one year before Queen Victoria began her reign.

The stock has increased by just 4% in 10 years. As such, maybe doctors could prescribe it as a cure for insomnia!

So why did I invest more money in this ‘boring’ share a few weeks ago?

Ex-dividend drop

For the record, I bought 458 shares in March for £2.45 each. These cost £1,125 before stamp duty.

The position was up around 12% until last week when the stock dropped 6.4% after going ex-dividend on 23 April. In other words, it’s currently trading without the right to the next dividend, which will be paid on 4 June.

And therein lies the main reason why I invested: passive income. From these 458 shares, I’ll receive £71 in June, then another £28 or so in September (unless there’s a shocking cancellation of the interim dividend).

When I invested then, the dividend yield was a juicy 8.8%. And it’s still around that level on a forward-looking basis, making L&G the highest-yielding stock in the FTSE 100.

More than income

Beyond dividends though, there were a couple of other reasons why I bought more shares.

First, under CEO António Simões, the company has committed to more share buybacks. For example, it recently announced a £1.2bn buyback (the largest in its history), funded partly by the sale of its US insurance unit.

Buybacks reduce the number of shares in circulation, which can boost the earnings per share (EPS) metric. And I hope this might give the share price a kick up the backside over the next couple of years.

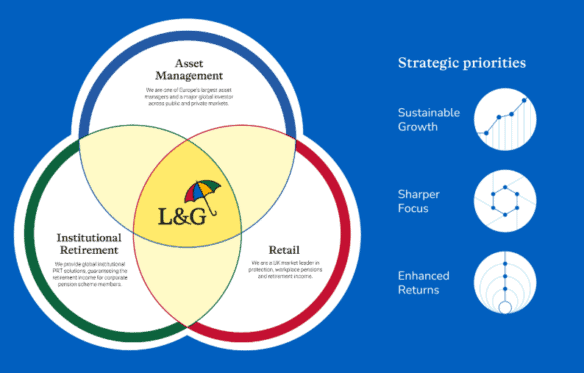

Also, in a bid to make the group simpler and easier to understand, L&G has been reorganised into three divisions. These are Asset Management (one of Europe’s largest asset managers), Retail (personal pensions, life insurance, etc), and Institutional Retirement (pension risk transfers).

This reorganisation aims to “shift towards fee-based earnings at higher returns on capital“. Longer term, the UK is set to have an ageing population, which should be fertile ground for leading pension providers like L&G.

Not without risk

The company obviously manages a massive quantity of bonds (fixed-income assets) to back annuities and insurance liabilities. As a result, sudden bond market volatility can distort reported profits.

Another risk to profits would be a prolonged economic downturn in the UK. That could see significant value wiped off its commercial real estate and residential assets, as well as result in less activity in its retail division.

Finally, another long-term challenge is longevity. If new AI-driven medical breakthroughs significantly increase life expectancy, L&G will have to pay out pensions for many more years than originally calculated.

Worth the risk?

To cover its generous dividend, the firm needs earnings growth to pick up over the medium term. However, the near term looks more certain, with the company already committed to 2% annual dividend growth through 2027.

On balance, I think the stock’s worth considering for the ultra-high-yield passive income it’s currently offering.

Source link