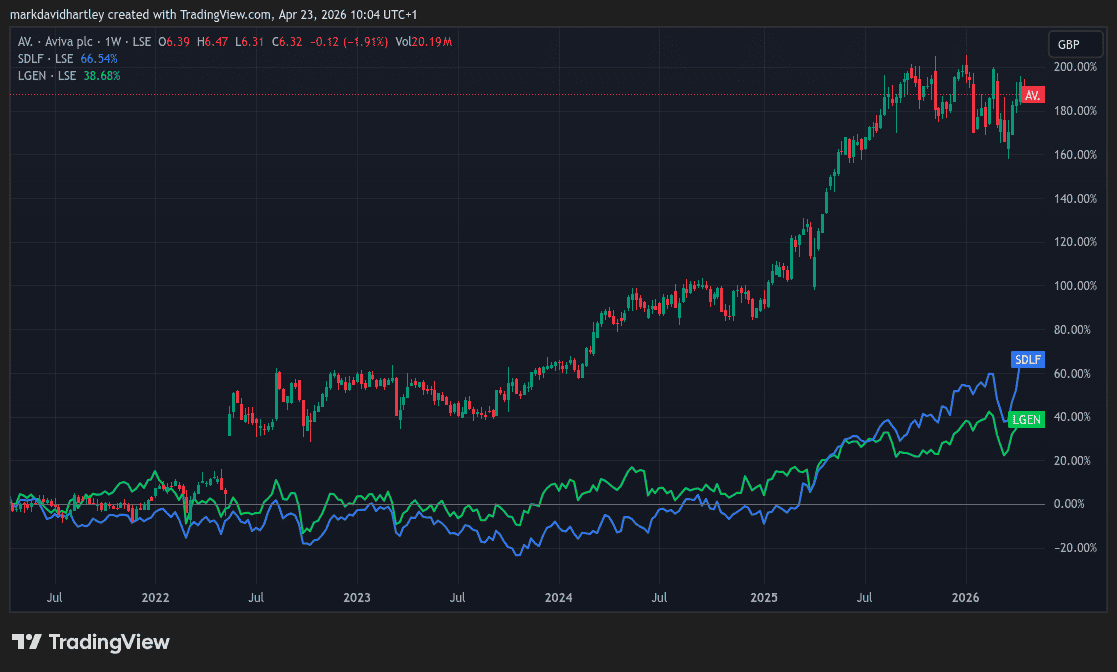

The Aviva (LSE: AV.) share price has increased by 60% over the past five years. Okay, it’s no Rolls-Royce — but it’s considerably better than rivals Legal & General and Standard Life.

And that’s just the price growth — when adjusting for dividends, the total return is closer to 187%. It means shareholders that reinvested all dividends would have netted an annualised return of 23.7% a year since April 2021.

That’s almost triple Standard Life’s 66.3% total return in the same period. So does that mean investors missed the boat? Not necessarily. Looking at value metrics, Aviva doesn’t look horribly overvalued. Here’s why…

Earnings visibility

The value of a company can’t be directly interpreted using the share price alone. Many penny stocks are exceptionally valuable, while some high-price tech stocks aren’t worth half their listed value.

Accurately assessing a stock’s value is no easy task and relies on the accuracy of earnings projections. When a business has a solid pipeline of orders or multi-year long contracts, this is easier to do.

When it comes to insurers, it’s important to assess a few key factors, including:

- Solvency coverage.

- Premiums.

- Earnings growth.

- Cash flow.

- Balance sheet health.

In Aviva’s case, its Solvency II cover ratio dropped to 180% after the recent Direct Line acquisition. However, a reported £350m in savings is expected to help it improve over time.

More importantly, the business is targeting annualised earnings growth of 11% over the coming three years. Considering profits rose 25% in 2025, this seems like a realistic target.

Income appeal

Good value aside, for income seekers, Aviva’s dividend story is arguably the main attraction. The total dividend per share for 2025 was 39.3p, up 10% on the prior year, and the company’s guided to ongoing growth.

The yield’s remained steady at roughly 6.2% for the past year, higher than most FTSE 100 names (but admittedly lagging key rivals). Coverage is thin but the 41-year-long track record helps quell any fears of a pause.

Plus, the recently rebooted £350m share buyback programme adds high conviction, supported by strong earnings and cash generation.

Still, the risk of rising claims inflation is a key concern. Higher costs for repairs, medical treatment or weather-related payouts can squeeze underwriting margins, especially in general insurance.

About a quarter of Aviva’s profits come from motor claims alone. If they outpace premium increases, earnings take a hit, which has been a significant challenge for insurers lately.

The bottom line

The income story remains the core selling point for Aviva, even though recent growth has turned heads. But dividends mean little if the share price drops faster than they pay out. That’s why it’s important to avoid overpriced stocks or you could risk getting stuck in a value trap.

Macro challenges mean Aviva probably won’t achieve the same returns in the next five years, but the valuation doesn’t point to significant risk of a downturn either.

So for investors looking for a solid dividend compounder in a long-term ISA, it remains a good option to consider. That said, recent geopolitical developments point to stronger growth opportunities elsewhere on the FTSE…

Source link