Image source: Getty Images

Opportunities to buy stocks like Netflix (NASDAQ:NFLX) at attractive valuations are rare. But it’s a business I’m very keen to own in my ISA.

It’s 30.68% off its all-time highs, but it still doesn’t exactly scream value. Is it cheap enough for me to buy?

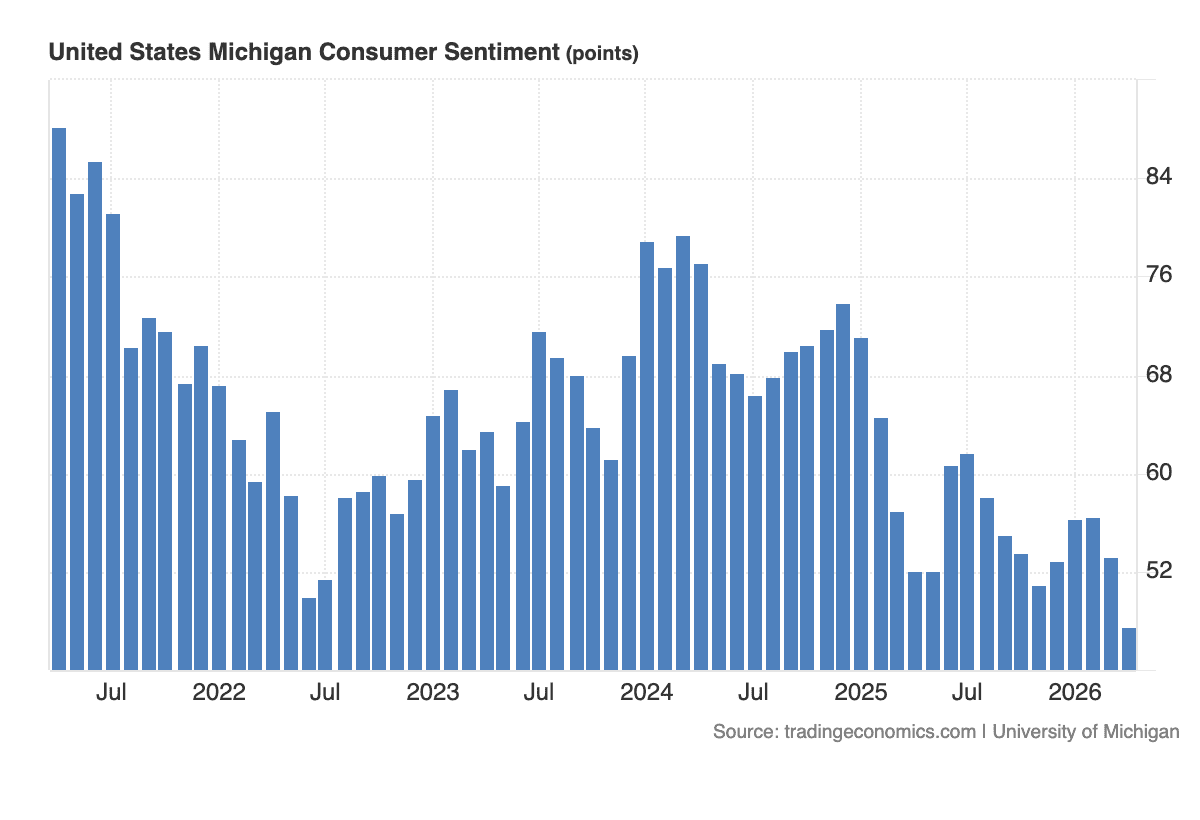

Consumer sentiment

According to the latest data from the University of Michigan, consumer confidence is at a five-year low. And that makes sense.

Source: Trading Economics

Mortgage rates are high, fuel prices are up, and artificial intelligence (AI) is threatening job security. On the face of it, that should be a risk for Netflix.

With budgets being under pressure, people might think about cancelling subscriptions. But I think the opposite’s more likely. While I expect households to cut spending, I don’t see Netflix as an obvious casualty.

It offers a lot of value at a modest price. The firm’s most expensive tier is $26.99 a month. Compared to going out pretty much anywhere, that’s not expensive.

My suspicion is that those looking to pull in their spending might see it that way. Especially with cheaper tiers available.

Assets

Another risk with Netflix is its ongoing costs. The firm has to keep producing content and this involves guaranteed costs with uncertain returns.

The company tried to buy Warner Bros Discovery (WBD), but that didn’t work out. I think though, that might be a good thing. WBD has top-quality franchisees. That however, is no guarantee of success, as various owners of those assets have found.

Netflix’s rival Paramount Skydance is set to pay $110.9bn for WBD. But it isn’t obvious to me that the firm can afford this. It’s a huge risk for Paramount. And I think Netflix might have been wise to let them take it – and claim a $2.8bn termination fee.

The situation reminds me of Teladoc Health buying Livongo in 2020. But if I’m right, then Netflix is the real winner here.

Outlook

Netflix’s latest guidance fell short of Wall Street’s expectations. Revenues and margins for Q2 were below analyst forecasts. That’s a reflection of the two risks facing the company. Importantly however, engagement remains high.

It’s the most popular streaming service behind YouTube by some way. And this is what I think ultimately matters.

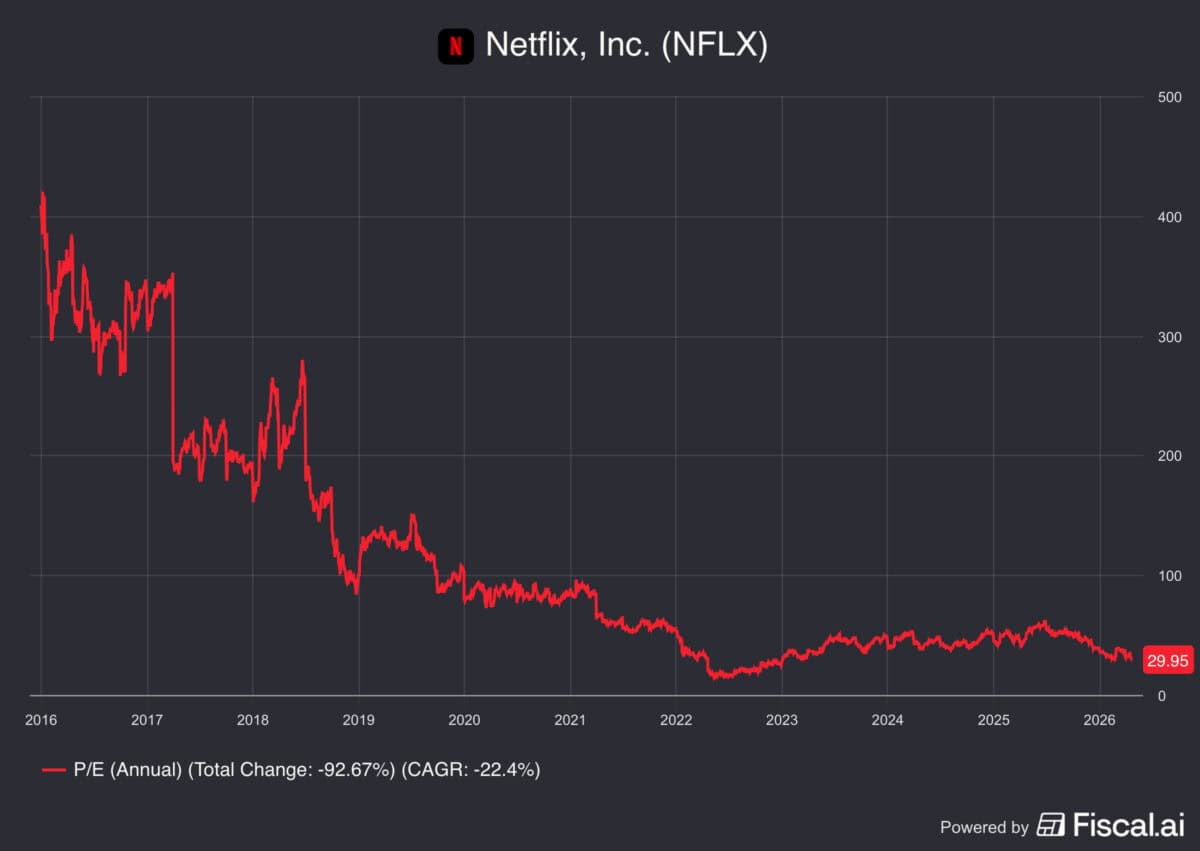

Officially, Netflix shares are trading at a price-to-earnings (P/E) ratio of 30. That’s above the S&P 500 average, but is it cheap enough? It’s not where the stock was when the firm reported declining users in 2022. But chances to buy it at this level have been rare.

Adjusting for that $2.8bn windfall though, the P/E ratio is closer to 37. And that might be a touch high for a huge opportunity.

Is this my chance to buy?

I think Netflix is doing well and I see the firm as the real winner from the Warner Brothers Discovery deal. So should I buy the stock?

I have two thoughts. One is that I might not get a better opportunity – it’s trading at some unusually cheap multiples at the moment. The other however, is that I think I can see more compelling opportunities right now. So I’m watching closely, but I’m buying elsewhere.

Source link