Image source: Getty Images

Rolls-Royce might attract more fanfare, but Fresnillo (LSE:FRES) shares have minted investors a fortune over the past year. In this time, they’ve soared 243%, with cascading dividends on top.

However, the FTSE 100 stock has come off the boil recently. In fact, anyone who invested £5,000 in Fresnillo just five weeks ago would have lost around £850 following a 17% pullback.

From a peak of 4,448p in January, the stock has now fallen 26% to 3,250p. Does this dip present a buying opportunity to consider?

Operating leverage

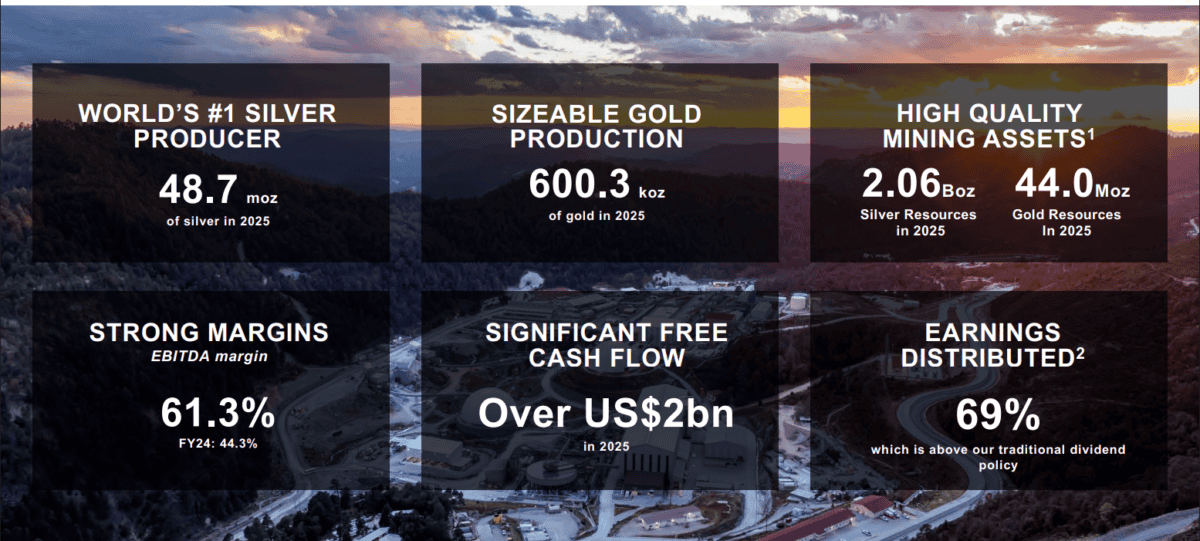

For those unfamiliar, Fresnillo is the world’s largest silver producer and Mexico’s leading gold miner. It owns a portfolio of high-quality assets, with over 2bn ounces of silver resources and 54m ounces of gold.

Last year, revenue jumped 30.5% to $4.56bn, while net profit skyrocketed 594.3% to $1.57bn. And this despite production volumes actually declining (silver and gold fell 13.5% and 5%, respectively).

So why did profit grow nearly 20 times faster than revenue? Well, this is a classic example of operating leverage in the mining sector. As gold and silver prices have soared, Fresnillo has benefitted from covered fixed costs, meaning extra revenue has basically dropped straight to the bottom line as pure profit.

This enabled the Mexican miner to dish out $950m in dividends to shareholders last year, a record amount. Adding these in, the 12-month total return is approximately 275%.

CEO Octavio Alvídrez commented: “These results demonstrate our ability to leverage our high-quality asset base while managing costs carefully to expand margins, resulting in significant cash generation and returns to our shareholders.”

Is the bull run over?

Precious metals have been on a historic bull run, driven higher by various factors. These include:

- Global economic instability

- Geopolitical tensions

- Central banks buying gold aggressively

- Record global government debt

- Supply constraints

- Industrial demand for silver

For Fresnillo, the question now is, will gold and silver keep soaring? Well, I don’t have a crystal ball to know where commodity prices are heading in the short term. If gold and silver keep falling, then so will Fresnillo’s share price. This is the obvious risk here.

However, I think most of the structural drivers mentioned above are still very much intact. Take sovereign debt. When money is printed to service debt, the purchasing power of fiat currency drops. Gold and silver, which obviously cannot be printed, act as a sort of insurance policy against this debasement.

From what I see, governments in the West currently have little appetite to reduce public spending. Meanwhile, silver has rising industrial uses in solar panels, electric vehicles, and defence applications.

Gold has hit record highs in the period, reflecting geopolitical tensions, while we are also seeing a strong underlying support from central banks. We expect these themes or aspects to continue for the foreseeable future.

Fresnillo

Dividend yield

The stock’s offering a decent 3.6% forecast dividend yield. And following another production dip this year, the miner expects gold and silver volumes to bounce back in 2027 and 2028.

A recent acquisition in Canada has added another 10m ounces of gold to its resource base, while the balance sheet is in tremendous shape.

For investors with a stomach for volatility, I think Fresnillo is worth considering after its 26% fall.