Image source: Getty Images

Billionaire investor Warren Buffett has a brilliantly simple approach to investing. Focus on the underlying business instead of the share price and be greedy when others are fearful.

These seem like obvious principles. But it’s surprising how much of an advantage investors can glean just by sticking to these in a stock market crash.

Stock market threats

Right now, investors have plenty to worry about in the stock market. There’s the ongoing risk of artificial intelligence (AI) leading to job losses and putting pressure on consumers.

That might show up in a few different places. Lower discretionary spending is one example and another is an increase in mortgage defaults is another.

More recently, conflict in Iran has added another dimension. Rising oil prices are set to bump up costs for heavy industrial businesses that have high power needs.

Some companies though are more at risk than others. And a stock market crash can give investors the chance to buy shares in quality companies at very attractive prices.

Opportunities

Buffett’s initial Bank of America deal is a great example of being greedy when others are fearful. With the bank in financial trouble in 2011, Buffett arranged a $5bn investment.

In return, his investment vehicle Berkshire Hathaway received 50,000 shares of preferred stock, which came with a 6% dividend. It also received warrants to buy 700m ordinary shares at $7.14.

In 2017, Buffett used the warrants to buy a stock that was trading at $24 per share using the original preferred stock. So the initial $5bn turned into almost $17bn in one move.

Realistically, investors like me are highly unlikely to be in a position to do that kind of deal in the next stock market crash. But I think there will be opportunities for those who are looking for them.

Where I’m looking

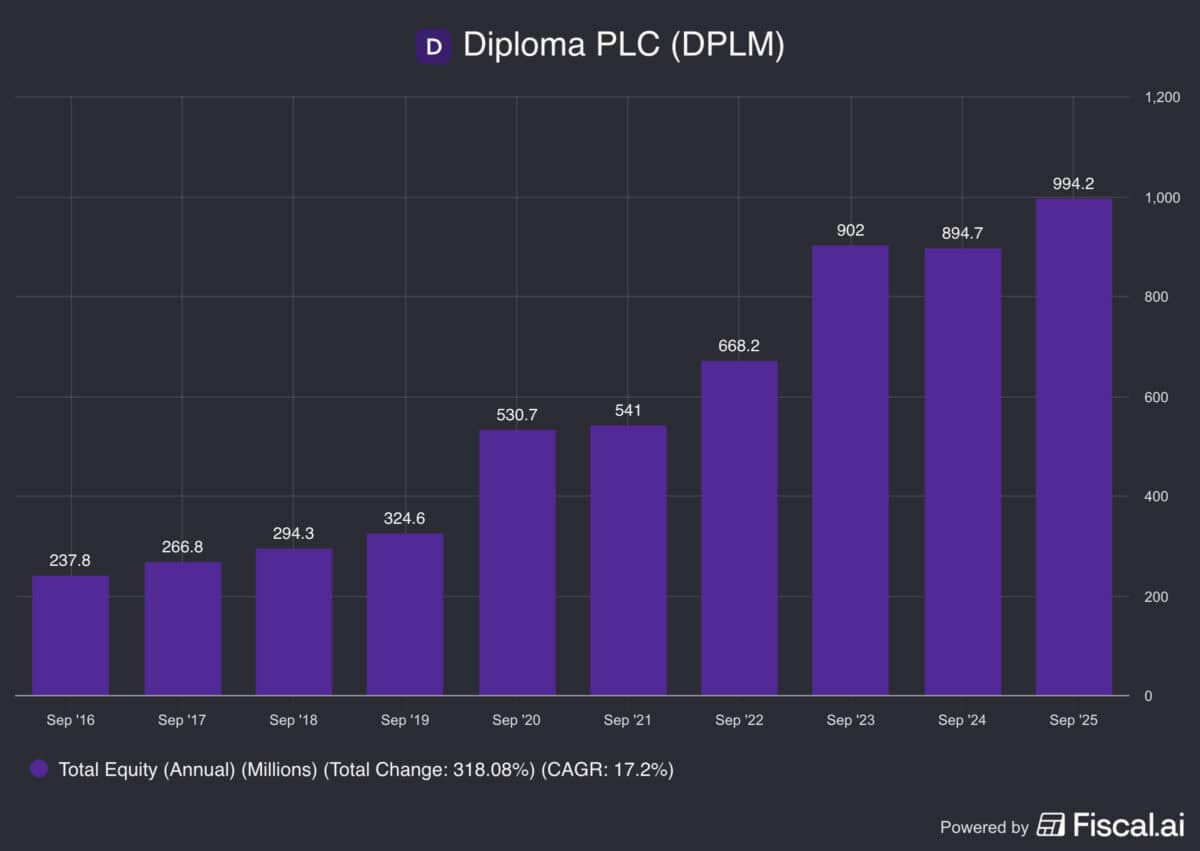

One stock I’m keeping a close eye on is Diploma (LSE:DPLM). The industrial distributor is an extremely high-quality business that looks expensive right now – but that could change.

Acquisitions are a key part of the business model and this brings a risk of overpaying. And the company has been paying higher prices recently, which is worth keeping an eye on.

Despite this, the firm’s record is outstanding. With Diploma retaining most of its cash (instead of paying dividends) changes in book value are a key metric to focus on in terms of growth.

From this perspective, the last 10 years have been a huge success – annual growth has been 17% on average. And I think there’s more to come, but the issue right now is price.

Buying

The thing with Diploma is that its growth hasn’t been linear. But whenever it looks like it might be stalling, a high price tag means the share price can fall sharply.

When book value stagnated in 2021, the stock fell 35% in the first half of 2022. And it fell 21% in early 2025 after a steady, but unspectacular, performance in 2024.

I’m sure this will happen again and I’m looking to be ready when it does. But a stock market crash might also do the job just as well in terms of generating an opportunity for me.