![[original_title]](https://rawnews.com/wp-content/uploads/2024/09/Portfolio-Review-Investor-with-High-Anxiety-Page-2.png)

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

Half 2:

Up to date on Sept 4, 2024I need to begin out by saying that I actually respect everybody that has helped me on this discussion board. Your assist, knowledge, and the time you set in for a stranger/rookie investor didn’t go unnoticed. Thanks a lot. I most likely spent a mean 30mins to an hour per put up (some longer), simply so I can perceive everybody’s recommendation higher. With that being stated, I need to share the progress I’ve made, however there may be nonetheless some extra work to be accomplished:

Glad to listen to you bought helpful suggestions and hopefully we are able to proceed offering useful concepts in your persevering with funding selections.

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

a) With everybody’s suggestion, I’ve modified my Desired Asset Allocation:Desired Asset allocation: 80% shares / 20% bonds

Desired Worldwide allocation: 30% of shares

A leap out of your part-1 AA of 60/40 to your part-2 AA of 80/20 is definitely extra aggressive. I am going to say that is advantageous for a pair each age 41, however my solely warning is that needs to be primarily based on your joint risk-tolerance and never as a result of “everybody’s suggestion” was that you just be extra aggressive. AA is about your “sleep properly at evening” issue and has the least affect in your steadiness at retirement; how a lot you contribute and the way lengthy you make these contributions is a a lot, a lot bigger affect than AA, so simply be certain that is best for you (not as a result of some Boghleads stated so) and that you just will not panic-sell if the inventory market crashes -50% and your portfolio drops -40%. I am emphasizing this as a result of your unique title included the adjective “excessive anxiousness,” which was hopefully nearly not realizing what to do subsequent slightly than watching your cash evaporate in a crash after which most likely get well properly earlier than you retire.

In case you’re fairly comfy with the volatility of an 80/20 portfolio (and I do assume that is advantageous for a pair of 41y olds), then nice! In case you picked 80/20 as a result of that appeared to be a consensus of what others have been saying you must maintain, then I feel you must do one or each of the workout routines under to verify that this new AA is acceptable for you and your partner.

1) Learn the Wiki article for Assessing Risk Tolerance, take the Vanguard Investor Questionnaire, then tailor the asset allocation (AA) that was really useful by the quiz primarily based in your information of your private threat tolerance having learn the Wiki article.

2) Alternatively (or along with), ask “How a lot of a drop in portfolio worth as a % of complete worth can I deal with?” reduce that % in half to get commonplace deviation, then lookup that std. dev. on the X-Axis of the chart under, and eventually scan as much as see what AA that corresponds to. For example, should you can solely abdomen a -24% drop in portfolio worth, that is a ±12% std. dev, which corresponds to an AA of 60/40. The return you get is a mean and you will get what you get along with your distinctive sequence of returns (there’s lots of variance in outcomes because of the related volatility of shares so it most likely will NOT be the typical, however one thing kind of).

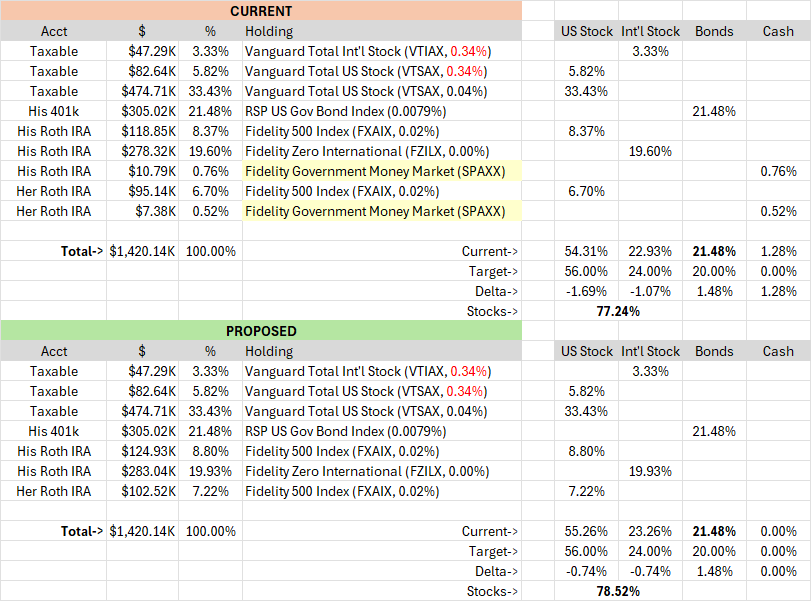

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

b) Approximate dimension of complete funding portfolio under($1.42mil). I even have an extra $200k (HYSA – Capital One 360) that I didn’t embrace under, however I’ll need to make investments finally. Any suggestions for the setup under?

Your setup seems to be nice to me! It adheres to tax-efficient placement and there is not any wash sale points that I can see. You might be brief on bonds by -1.48%, however that can seemingly be fastened over time as he continues to make 401k contributions to the bond fund. The proposed part is a suggestion on how the money ready to be deployed (light-yellow spotlight from latest Trad->Roth conversion) in His Roth IRA may very well be break up amongst US and Int’l inventory such that the error relative to the goal AA is about the identical (assumes her Roth IRA money would go to Fido 500 Index).

You might be paying for Vanguard Private Advisor Choose (VPAS), but it surely’s just for about 9% of your portfolio; are they making suggestions (just like the 529 contribution) outdoors of the portfolio which might be definitely worth the 0.30% charge to you (which I feel is added to the underlying fund ERs, so 0.34% slightly than simply 0.30%)? In the event that they’re making funding portfolio suggestions, do they learn about all of your different holdings? If they’re however do not learn about your complete portfolio then they may present recommendation that is smart for the 2 funds they see, however which within the context of the complete portfolio of accounts doesn’t make sense. Simply one thing to concentrate on once you take recommendation out of your advisor that won’t have a whole monetary image.

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

c) I’ve modified His 401k contribution to Pre-tax, as an alternative of After-tax. Shifting ahead, I plan to max out my Conventional 401k first, then use After-tax 401k.

That is seemingly advantageous because it offers you a direct tax-break now and you’ll all the time do Roth conversions in retirement however earlier than you acquire SocSec, once you may be in a decrease tax bracket. I feel it is a good aim for placement flexibility to have Taxable, Tax-Deferred, and Tax-Free balances which might be fairly comparable greenback quantities on getting into retirement, slightly than one account sort dominating the opposite two. Nonetheless, that always occurs with the 401k being largest (or generally Taxable being largest for very excessive earners) and is addressed by Trad to Roth conversions in early retirement.

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

d) I’ve zero out my Rollover IRA and transfer the funds into my Conventional 401k to eradicate an account. This additionally permits me to do a Backdoor Roth IRA, which for 2024, I’ve contributed $7k to my spouse’s Backdoor Roth IRA, and $7k to His Backdoor Roth IRA.

This was a great transfer to allow backdoor contributions to His Roth IRA!

Is that this sufficient for 6-18 months of bills (not internet earnings) if certainly one of you is unexpectedly laid off? The particular time needs to be matched to how lengthy it might seemingly take to discover a alternative job at comparable wage (greater wage usually means an extended job hunt). This is perhaps advantageous (or much more than sufficient) should you can in the reduction of on discretionary spending and reside on simply the lesser of the 2 salaries (assuming your not each working for a similar employer).

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

1) His 401k contribution is at the moment set for RSP US Gov Bond Index_(n/a)(0.0079%) each month. This may unbalance my Asset Allocation extra on the bond facet if I contribute to it $3k+ each month. What ought to I concentrate on with my 401k contribution? Is there one other funding I ought to think about in my 401K account additionally if the Bond AA is simply too excessive, and in that case, which one?

Since contributions to the 401k may very well be as much as $23K/yr whereas Roth IRA is proscribed to $7K/yr, sure you will finally need to divert your contributions from 100% into bonds to a inventory/bond break up (say 80% shares, then 20% bonds to begin on paper then modify primarily based on what you assume the year-end contribution imbalance can be throughout all accounts). You needn’t assume too arduous or fear an excessive amount of on this, since you might simply repair it in your annual or quarterly rebalancing (i.e., simply go away contributions 100% bonds, 80/20 break up, or 100% shares, or no matter after which in your rebalancing date, shift some bonds into shares, or vice-versa, contained in the 401k to deliver the overall portfolio throughout all accounts again heading in the right direction).

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

2) I at the moment have two investments (approx. $130k) in my Joint Taxable at Vanguard which might be beneath the Vanguard Private Advisor Choose Portfolios (expense ratio = 0.3% + $75 quarterly charge). I attempted to name them to cancel the service, however they transferred me to their retention specialist, and he satisfied to remain. His gross sales pitch was that I can name to an Advisor for assist if wanted. Ought to I name again in to cancel it, and simply transfer the 2 funds to a non-advised account?

This goes again to my earlier query about whether or not this 0.3% charge is “value it to you.” What recommendation are you getting that you might not get right here or discover by yourself with just a little net analysis? Does gaining access to a CFP (for simply 9% of your complete portfolio, so maybe not that massive a value) offer you peace of thoughts to cut back your excessive anxiousness? In my first response to your unique put up, I stated that such anxiousness can result in bodily stress which might trigger well being issues (or exacerbate current ones), so if having knowledgeable CFP to speak to helps keep away from well being points, I might say that was value it to me, however this can be a private alternative you should resolve. Many DIY Bogleheads will let you know to ditch the advisor and save the prices however that is them and their high-confidence, zero-anxiety, expertise with self-managing their portfolios… should you get that response from others, think about how your expertise (or lack of) and concern differs from these which might be providing you with recommendation to ditch the advisor.

The opposite factor to make clear (or negotiate) is the Private Advisor Choose (PAS) price. PAS requires $500K, however you solely have $130K beneath administration with PAS, so the additional $75/qtr ($300/yr) is more likely to compensate for the truth that you do not have a minimum of $500K “beneath administration,” however they let you’ve got entry to a devoted CFP for this nominal cost as a result of you’ve got $600K “at Vanguard.” So in complete your devoted CFP is costing you slightly below $700/yr ($129,930 x 0.30% + $300 = $690). Only for comparability towards different advice-only advisors, Rick Ferri costs about $1,000 for preliminary session & planning, then $450/hr for follow-on consulting; Mark Zoril (of Plan Imaginative and prescient) costs one thing on the order of $300 for setup, however then a decrease annual “upkeep” price (I am not recommending both of these, they’re merely cited for price comparability).

To be clear, I additionally would ditch the advisor in a heartbeat, however I’ve high-confidence and zero-anxiety, in order that’s me, not essentially you.

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

3) For the $200k in my HYSA (Capital One), how ought to I begin investing it? Ought to I dive proper in, and embrace it with my Asset Allocation plan (80 inventory/20 bond)? Ought to I slowly use it to feed our Backdoor Roth yearly? Ought to I exploit it to assist rebalance my portfolio if wanted?

You possibly can seemingly make investments it immediately in your joint Taxable account. Taxable accounts needs to be 100% shares per tax-efficient placement, so it may very well be break up amongst VTSAX and VTIAX to try to maintain your AA on monitor (your bond allocation will fall just a little behind however that can catch up shortly with $3K/mo contributions to His 401k). I say “immediately” as a result of lump-sum beats DCA 67% of the time, however should you’re in any respect nervous and/or would have important remorse if the market have been to appropriate/crash simply after you made a lump-sum funding, then think about solely lumping in half after which DCA the opposite half into joint Taxable over 6-12 months. Once more, it is a private name that it’s a must to resolve.

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

4) Is there a rule of thumb on when to rebalance the portfolio? Is it each 3 months, or is it when the Asset Allocation is off by 5%+?

There’s an both/or in your chosen periodicity (private alternative of month-to-month, quarterly, or yearly) -OR- every time the allocation is off by greater than some threshold (±5% is usually really useful). See the Wiki subject on Rebalancing Approaches.

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

5) Simply curious, what’s the distinction between the three bond funds choices (RSP US GOV BOND INDX (0.0079%), RSP BOND INDEX (0.0262%), RSP SHORT TERM BOND (0.0181%)) in my 401k, and why was RSP US GOV BOND INDX really useful over the opposite bond funds? Do I would like to fret about bond funds with the rate of interest fluctuating up and down?

Simply wanting on the fund names, I might say GOV BOND is just US Treasuries & Gov’t-backed Mortgages, whereas BOND INDEX is probably going extra like a Complete Bond Fund that has each Gov’t debt and company debt; each of those are seemingly intermediate time period (avg. period round 6-7 years), whereas SHORT TERM BOND, is because the identify implies brief slightly than intermediate (much less volatility and decrease yield). GOV BOND is the bottom price amongst these three, in order that is perhaps driving the advice; all three are seemingly appropriate you probably have a desire. I feel worrying about fluctuations in shares and bonds is just not a fruitful expenditure of emotion… you may’t management what occurs, you may solely react if there is a massive change by rebalancing your portfolio to keep up your threat profile.

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

6) Is there a greater place to stash majority ($40k) of my emergency fund as an alternative of leaving all $60k in my checking account?

Since you’ve got a joint account at Vanguard and Vanguard’s MMF charges are typically higher than Schwab & Fido, I might counsel transferring the quantity you need to maintain outdoors checking to the Taxable account, after which investing it in VUSXX @ 5.23% however exempt from CA taxes, so a Tax-Equal Yield (TEY) of 5.23% / (1 – 9.3% CA) = 5.77%, so higher than the settlement fund (VMFXX) at 5.25%. I solely maintain $5K in my credit score union financial savings account as I can get by way of a month of bills on that; all the remainder of my EF was within the VMFXX since I can transfer cash between VMFXX and my checking account in about 2-3 days, so I noticed no have to maintain that a lot money in checking/financial savings (incomes primarily nothing). $20K retained in checking is okay, if that is what you are comfy with, however you might most likely maintain a lot much less there (sufficient to pay all month-to-month payments that converge on a due-date in the identical week, so you’ve got time to maneuver money from MMF to checking).

SacramentoInvestor wrote: ↑Mon Jul 29, 2024 1:51 am

7) The advisor from Vanguard Private Advisor Choose Portfolios crew really useful that I put a one-time $10k contribution into every of my youngsters 529 accounts. This manner, their 529 can probably double by the point they go to school. The funds would come from my HYSA. Is that this really useful?

This looks as if an affordable suggestion. If $10K have been to double (that is solely a “potential” development case, however not an unreasonable expectation), then there’d be $20K within the 529, which is under the $35k lifetime rollover restrict to a Roth IRA if the funds are NOT used for training bills (i.e., the kid opts out of pursuing a level program). Some folks load up their 529s with significantly extra belongings (sufficient to pay for almost all 4 years of faculty), since if used for training the expansion is tax-free, and I am certain a lot of these take pleasure in that profit, however there’s all the time the chance that your youngsters simply aren’t excited by school, regardless of all of your greatest efforts to persuade them it is a profession benefit (esp. should you’re paying for it they usually do not graduate saddled with $100K to $400K in debt).

Maybe the advisor has this in thoughts and is making an attempt to maintain 529 accounts beneath the $35K rollover restrict within the occasion that they are not used (you may nonetheless get the cash if they do not go to school, however funds in extra of $35K have a ten% non-education penalty plus taxes on earnings at strange earnings tax charges, which is fairly stiff in comparison with tax-free rollover to a Roth). I are likely to agree with the advisor to maintain complete development in 529s to $35K and put the rest of funds in direction of school in UTMA accounts or your individual Joint Taxable account.

Do not do what Bogleheads let you know. Hearken to what we are saying, think about different sources, and make your individual selections, since it’s a must to reside with the dangers & rewards (not us or anybody else).